At Truevo, we talk a lot about processing transactions, optimizing checkouts, and boosting acceptance rates. But behind the scenes, a massive part of our daily operation involves managing risk.

For many e-commerce business owners, the risk management side of an acquirer can feel like a “black box.” You submit your application or process your weekly volumes, hoping everything looks good, but you aren’t entirely sure what we are looking for.

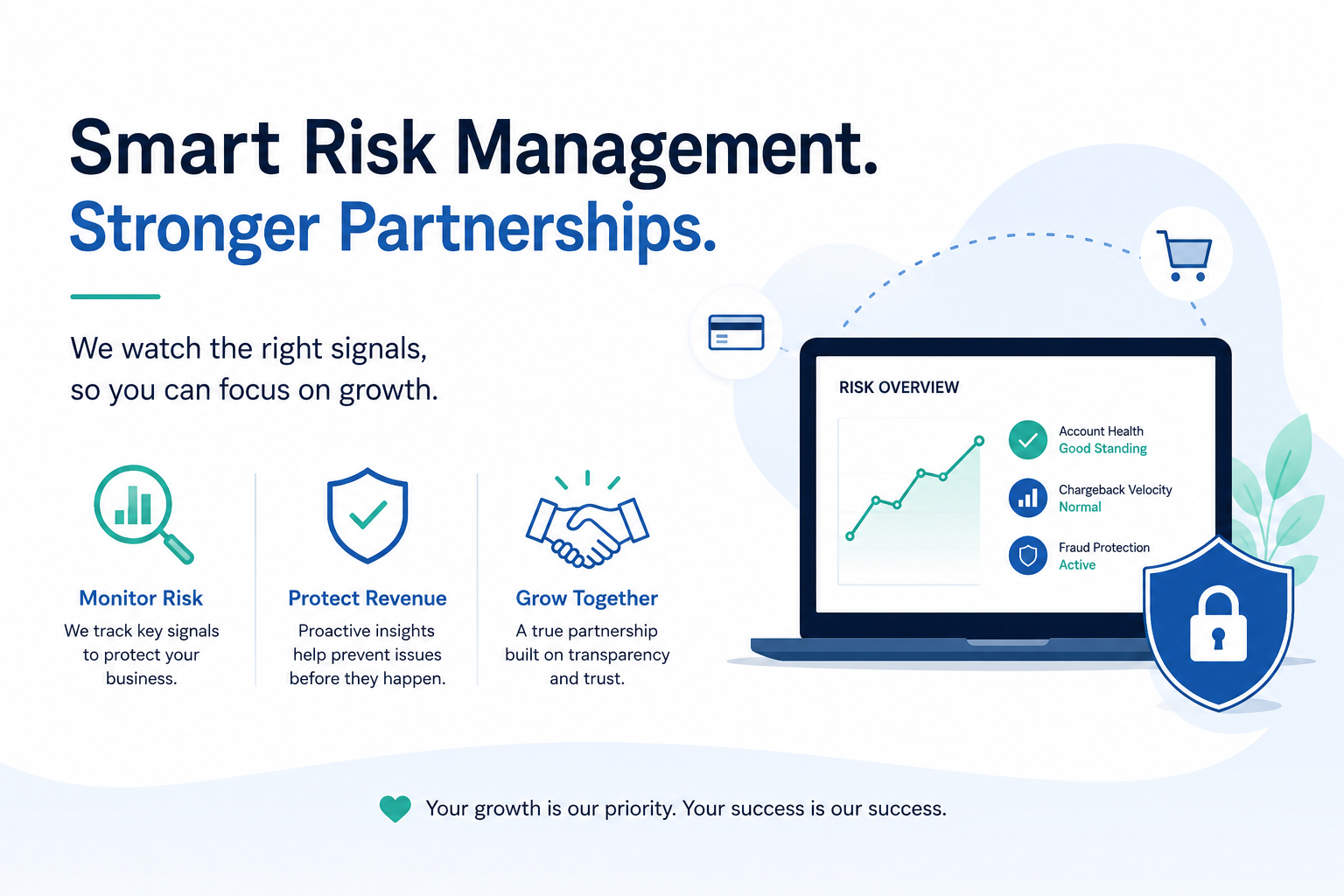

To pull back the curtain, we sat down with our risk and underwriting teams to answer some of the most common questions merchants ask us about risk signals, account health, and what it takes to build a bulletproof partnership.

Q: “What merchant risk signals do acquirers watch most closely?”

A: When we look at a merchant’s account health, we aren’t just looking at the total revenue you generate. We look at operational patterns that signal whether a business is stable or hitting a rocky patch.

The three biggest risk signals on our radar include:

- The Velocity of Chargebacks (and Disputes)

It’s a common misconception that acquirers only care if you hit the official Visa or Mastercard chargeback threshold limits (usually around 1%). In reality, we watch the velocity—how fast your chargeback rate is rising over a 30-day period. A sudden spike usually points to an underlying operational issue, like a bad batch of inventory, shipping delays, or a highly targeted fraud attack. - A Mismatch in Refund-to-Sales Ratios

Refunds are a normal part of retail, but if your refunds suddenly skyrocket while your overall sales volume dips, it triggers a red flag. High refund rates mean your capital is leaving the ecosystem quickly, which can create rolling reserve or liquidity issues if a business isn’t managed carefully. - Sudden Shifts in Ticket Size or Average Transaction Value (ATV)

If your online store typically sells €50 items, and suddenly you process a wave of €1,500 transactions, our automated risk systems take notice. This “ticket size anomaly” is a classic indicator of either card testing fraud or a drastic shift in your business model that wasn’t cleared during onboarding.

Q: “How can we keep our account in good standing if our business model changes?”

A: The absolute best thing you can do is over-communicate.

If you are planning a massive Black Friday flash sale, moving into a new geographic market, or introducing a completely new product line (especially if it’s a higher-priced item), let your account manager know before the traffic hits. When our risk team knows a surge is expected, we can adjust your profile parameters so our automated security systems don’t accidentally freeze your incoming funds thinking it’s a fraudulent anomaly.

Q: “What does a great Merchant-Acquirer relationship actually look like?”

A: A lot of businesses view their acquirer as a utility bill—something you pay every month and ignore until the power goes out. But in high-growth e-commerce, a great merchant-acquirer relationship functions like a strategic alliance.

Here is what a healthy, top-tier relationship looks like in practice:

- Transparency Over Hiding Data: If a merchant experiences a fulfillment crisis (e.g., a supply chain delay that will delay 500 orders), the best merchants tell us immediately. When you are transparent, we can work together on a proactive strategy—like setting up a temporary communication workflow for your customers—to head off chargebacks before they happen.

- Consultative Optimization: A great acquirer doesn’t just pass transactions through; they look at your data to help you save money. We should be actively reviewing your cross-border decline rates, suggesting local payment methods that could lift conversion, and helping you fine-tune your 3D Secure triggers to balance security with a smooth checkout.

- Shared Risk Accountability: We succeed when you succeed. A great relationship means our risk team acts as an extension of your team, helping you spot fraudulent patterns or malicious card-testing bots early, rather than simply penalizing you after the damage is done.

The Bottom Line

Acquirers aren’t compliance traffic cops trying to slow your business down; we are the guardrails designed to keep your financial infrastructure safe as you scale. By understanding the signals we watch and treating your payment processor as an expansion partner, you protect your revenue, keep your checkout uninterrupted, and set your business up for sustainable, long-term growth.